When Pharmacies Are Forced to Sell, Patients Pay the Price

By ALDP Co-founders Michael Glassner and Jason Young

Supporters of Tennessee Senate Bill 2040 and its House companion, HB 1959, have a reassuring answer for anyone who worries about pharmacy closures: divestiture doesn’t equal closure. A pharmacy that has to change owners, they argue, simply changes owners. The license transfers, the shelves stay stocked, and patients barely notice the difference.

It’s a tidy argument. It’s also incomplete. And for a specific group of patients, it may be dangerously wrong.

At Americans for Lower Drug Prices, we try to call balls and strikes. We’re not interested in worst-case scenarios designed to scare policymakers, and we’re not here to defend pharmacy benefit managers simply because some of the loudest voices opposing this bill happen to be PBMs. But a serious, evidence-based look at what pharmacy divestiture actually produces – in the market conditions that exist right now – leads to conclusions that legislators deserve to hear plainly.

All Pharmacies Are Already Under Pressure

Before evaluating what forced divestiture would do, it’s worth understanding the environment into which it would land. The American pharmacy market is under structural stress that predates this legislation by years.

CVS has closed roughly 900 to 1,000 stores since 2022 as part of a deliberate effort to right-size its retail footprint. Rite Aid, once a national chain, has essentially ceased to exist after twice filing for bankruptcy. Walgreens announced plans to close approximately 1,200 locations over three years and has sold itself to private equity. Independent pharmacies have been closing at a rate of several hundred per year, squeezed by declining reimbursement rates from PBMs, the rise of online competitors, and the slow erosion of the front-of-store merchandise sales that once helped sustain them.

Amazon, Walmart, Cost Plus Drugs, and Costco have all entered the prescription drug market in various ways, offering lower prices on common generic drugs and drawing cost-conscious consumers away from traditional pharmacy channels. This is, in many respects, good for patients who are shopping for price. But it compounds the pressure on the pharmacies that remain.

This is the baseline. The question isn’t whether a thriving industry can absorb a forced ownership change. It’s whether a distressed industry, with assets already under financial stress, can find willing buyers for scores of locations simultaneously, on a statutory deadline.

“Divestiture DOESN’T EQUAL Closure” Misses the Point

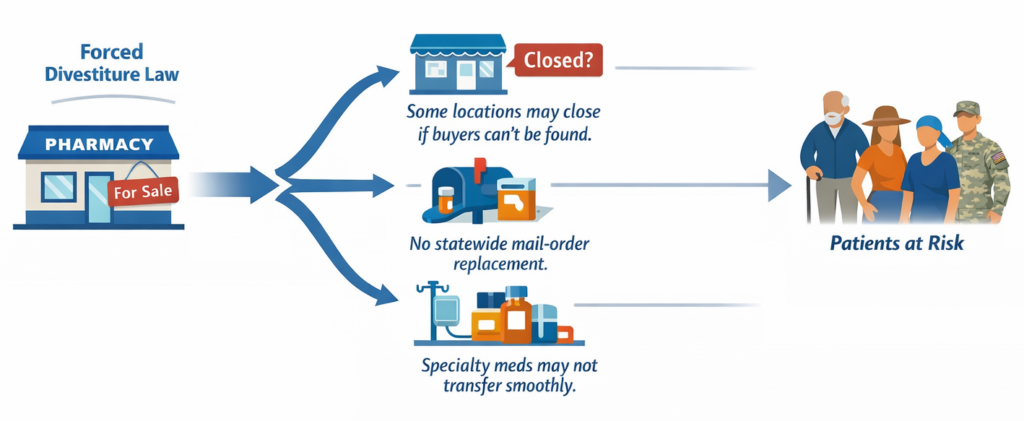

The claim that divestiture doesn’t equal closure is technically true. There is nothing in SB 2040 that orders a pharmacy to shut its doors. But it misses what actually happens in a forced sale.

When a seller is required by law to divest – on a fixed timeline, with a specific effective date – the negotiating dynamic shifts entirely in the buyer’s favor. A motivated buyer knows the seller has no choice. They can offer less, attach more conditions, and, if they’re a competitor, calculate whether they’re better off letting the clock run out and inheriting the prescription files after the seller exits the market entirely.

That last point matters. Walgreens, which operates 114 of its own stores in Tennessee, has no obvious incentive to help its larger rival CVS find buyers quickly. CVS’s complete exit from the market is, from Walgreens’ perspective, a favorable competitive outcome, not a problem to be solved. The same logic applies in reverse if the roles were switched. Expecting competitors to facilitate an orderly transition ignores basic market incentives.

Meanwhile, CVS itself is engaged in its own financial restructuring nationally. It has been closing stores, not opening them. There is no reason to expect it to invest resources in a graceful transition while it is still seeking buyers and preserving leverage.

The honest question isn’t whether someone could theoretically buy the 134 locations that CVS has publicly said would be affected by SB 2040 / HB 1959. It’s whether, given current market conditions, real buyers with real capital will complete real transactions by Jan. 1, 2027*, and what happens to patients in the locations where they don’t.

Mail-Order Is a Different Problem Entirely

Retail pharmacy closures would affect patients’ convenience and access. Mail-order disruption would affect a much larger number of patients in a more immediate way.

This is not an endorsement of the status quo, but rather a good faith effort to characterize it: PBMs’ mail-order pharmacies fill hundreds of millions of prescriptions annually for patients enrolled in employer-sponsored health plans, Medicare Part D, TRICARE, and Medicaid managed care programs. What Express Scripts, OptumRx, and CVS Caremark offer are not simple operations. They are large, automated fulfillment centers with proprietary software systems, controlled substance DEA registrations, and state-by-state pharmacy licenses.

An 11-month divestiture window* is almost certainly insufficient to find a buyer, conduct due diligence, negotiate a transaction, close it, and transition operations for a mail-order pharmacy of this scale. And critically, there is no obvious buyer. Walmart does not operate a scaled mail-order pharmacy. Cost Plus Drugs is predominantly a cash-pay, price-transparency platform, not a mail-order PBM replacement with insurance integration.

Patients who depend on mail-order for maintenance medications – blood pressure drugs, cholesterol medications, diabetes treatments – would be routed to retail pharmacies that are simultaneously absorbing the fallout from retail closures. It is a compounding disruption affecting a large population.

The Patients Who Can’t Just Find Another Pharmacy

And then there is specialty pharmacy, where the stakes are highest.

Specialty pharmacy is not simply a different size of pharmacy. It is a fundamentally different kind of operation. Specialty drugs – oncology biologics, multiple sclerosis (MS) treatments, hemophilia factor products, antiretrovirals, and many others – require cold-chain storage, disease-specific clinical expertise, and in many cases, direct contractual relationships with the drug’s manufacturer. These manufacturer agreements, called limited distribution arrangements, designate which pharmacies are authorized to dispense a given drug. They do not transfer automatically. Renegotiating them would likely take months.

The vast majority of independent pharmacies do not participate meaningfully in specialty dispensing. That’s not an accident; it reflects the capital requirements, the logistics infrastructure, and the specialized clinical staff these operations require. When a specialty pharmacy exits a market, there is no simple replacement. The patient whose cancer drug or MS biologic was dispensed by a pharmacy affected by SB 2040 cannot simply walk to the corner pharmacy or switch to mail-order. There may be no alternative that credentialed by their drug’s manufacturer or capable of maintaining the supply chain for their specific medication.

For these patients – people managing cancer, multiple sclerosis, rare diseases, and other serious conditions – a 30-day supply disruption is not an inconvenience. It is a clinical emergency that arrives wrapped in administrative language about licensure transitions.

A Less Competitive Market Means Higher Prices

There is a final dimension to this analysis that tends to get lost in debates about access: what happens to prices when the market restructures.

When specialty pharmacy volume concentrates into hospital-based dispensing – the most likely outcome when retail specialty pharmacy exits a market – patients often face higher out-of-pocket costs for the same medication. Hospital outpatient pharmacies operate under a different cost structure, with facility fees and administrative overhead that do not exist in retail pharmacy settings. The same drug, from the same manufacturer, covered by the same insurance plan, frequently costs a patient more when dispensed by a hospital pharmacy than by a retail specialty pharmacy. TennCare, small business owners, and taxpayers will pay more, too.

There is also the question of negotiating leverage. When, say, CVS Specialty is a going concern in Tennessee, insurers can negotiate dispensing terms against competitive alternatives. When the specialty pharmacy market contracts to fewer players, that leverage erodes. Remaining pharmacies can credibly demand better terms. Those terms flow through eventually to premiums and patient cost-sharing.

And in some cases, drugs that are currently self-administered at home – picked up at a pharmacy and injected by the patient – may shift to physician-administered versions in infusion suites if home dispensing becomes unavailable. This transition from the pharmacy benefit to the medical benefit is one of the most significant drivers of drug spending growth, and it produces dramatically higher costs for both patients and payers.

The result is a market that is less competitive by structure, with fewer dispensing options, reduced negotiating power for payers, and upward pressure on the prices patients actually pay. This is not a theoretical concern. It is the predictable economic consequence of a forced reduction in market participants.

What Policymakers Should Ask

None of this means that concerns about the PBM and pharmacy industries are illegitimate. They aren’t. There are real questions worth asking about whether PBM-affiliated pharmacies compete fairly against independent pharmacies, and whether patients’ interests are served by the current market structure.

But those questions deserve answers that are grounded in evidence and targeted at actual competitive harms. A forced divestiture bill with an 11-month implementation window*, no transition protections for patients, no buyer verification requirements, and no plan for mail-order or specialty pharmacy continuity is not a precision instrument. It is a blunt one. The patients most likely to be harmed by it are the ones least able to absorb the disruption.

The right questions for Tennessee legislators to ask are: Who, specifically, will buy these operations? On what timeline? With what continuity-of-care guarantees for patients who depend on specialty and mail-order pharmacy? What happens in February 2027* to the cancer patient whose specialty pharmacy has closed and whose limited distribution drug has no authorized alternative dispenser in the state?

Until those questions have credible answers, the “divestiture doesn’t equal closure” reassurance is not an argument. It is an assumption – and for some patients, a dangerous one.

* We published this post on March 8, based on SB 2040/HB 1959’s original text. Amended bill language was subsequently released, extending the divestiture deadline to Dec. 31, 2028 – adding up to 18 months to the compliance window. That extension is itself instructive: it suggests the bill’s supporters recognized that the original timeline posed serious risks to patient care and access. The amended language does not substantially change our analysis or our concerns. The fundamental questions we raise – about who will buy these operations and with what protections for patients who depend on specialty and mail-order pharmacy – remain unanswered.